On April 2, 2010 the Stanford Institute for Economic Policy Research released a policy brief entitled,

“Going For Broke: Reforming California’s Public Employee Pension Systems.” It was an interesting attempt to deconstruct the problems facing the taxpayers of California. It is in stark conflict with the official report.

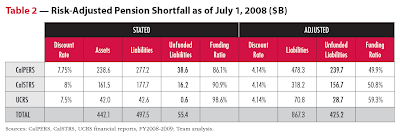

The officially stated unfunded liability of CalPERS at July 1, 2008 was $38.6 billion. Using the methodology of the Stanford graduate students it rises to $239.7 billion. Total pension obligations covered by CalPERS, CalSTRS and UCRS rise to almost $425.2 billion. In July of 2008 things still looked fairly good.

To calculate the amount of money necessary to fund a future liability a rate of return or discount rate is required. This is what an investment would expect to return over its lifetime. Using Excel enter a future liability (for example the cost of a child’s college education) enter the years until that obligation is due then guess on what your rate of return on an investment will be. The result is the

“present value” of that future liability. By subtracting the money actually available for investment from the present value of the liability the unfunded status is apparent.

In calculating a rate of return there are many opportunities. Let’s say you are

John Paulson , you might choose 20% or 100%. If you are the Social Security System you will choose U S Treasuries which return a lot less.

Here is where the mandarins of CalPERS sit while they calculate. They have come to the conclusion they will make 7.75%. Wikipedia points out their assets peaked in October 2007 at $260.6 billion and, as of December 2008, were down 31% to

$179.2 billion. Ooops!

What makes the brief from SIEPR important is its reflection on the appropriate assumed rate of return for a publicly funded pension plan. Case law in California establishes the immutable right of the employee to vested benefits. The brief argues that therefore the investment returns should likewise be immutable, in other words without risk of loss. And the place to go for that is U S Treasuries. While the brief was generous by assuming a return of 4.14% at 10 years (the available return at the time in U S 10 year Treasury Notes was 3.625%) it also points out a flaw in its own assumptions. The immutable returns to employees covered by CalPERS are indexed to inflation. As an alternative the Treasury also offers Treasury Inflation Protected Securities or TIPS eliminating inflation risk. On April 5, 2010 the U S Treasury auctioned 9 year 9 month TIPS Notes at a high yield of 1.709%. When calculating unfunded liabilities CalPERS assumes inflation will run 3%. I have suggested to

Joe Nation, the faculty adviser on the paper, a more appropriate rate might be the assumed inflation rate plus the TIPS rate. It still comes up to only 4.709%.

The Marin Municipal Water District is a microcosm of the State. As a participant in CalPERS, the value of pension assets rises and falls with the portfolio of CalPERS. In previous blogs I have outlined the problems faced by MMWD and estimated the total unfunded position at over $90,000,000. That number would pale to insignificance at a discount rate of 4.709%.

Pension liabilities accrue for a couple of reasons. First there are the promised benefits. Created by

legislation, written and sponsored by CalPERS in 1999, the road map was clear. In 1999 you can only imagine the heady feeling among the managers of California’s pensions. Approaching the peak of the tech bubble pension funds were swollen, overfunded to a degree unimaginable only a few years earlier. Contributions by participants were reduced and in some cases returned. It appeared the good times were here to stay and as a reward covered employees were granted extensive retirement benefits. For example the legislation established an accrual and retirement formula of 2% at 55. It means that for each year worked a benefit of 2% of the base, the average of the last three years salary, accrued and was fully vested at age 55. This became the standard for California public employees (other than safety employees who hold a special place in our hearts and received 2.5% at 50) and the assumed rate of return was 8.25%. Amid the economic turmoil of 2003 CalPERS reduced that rate to 7.75% where it stands today.

Markets rise and fall and by 2006 jubilation once again walked the halls of the Lincoln Plaza Complex at 400 “Q” Street. Buoyed by outsized investment returns and tax inflows from the housing boom, municipalities and agencies around the state upped the ante raising benefits to 2.7% at 55 for non safety employees and 3% at 50 for safety employees. Meanwhile union negotiators whittled away at the calculated base, the average of the last three year’s pay. Adding to the employees good fortune, boards charitably adopted only the

last year’s pay as the benefit standard, opening the way for well documented

abuses. Around the state ratepayers and taxpayers slept.

Once benefits are established the driver becomes investment returns. Again we consult with the mandarins, the managers of California’s retirement funds. The question of appropriate rates of return was the focus of a recent

interview with CalPERS Chief Investment Officer Joe Dear and Alan Milligan, CalPERS Interim Chief Actuary. Apparently immune from the randomness faced by the rest of the world Alan Milligan weighed in, "…as Actuaries, we need to know not just what’s going to happen in the next ten years, but also what is going to happen in the next 50 years.” In Alan’s world there are no

black swans. And if there are, well the taxpayers and the ratepayers are standing by.

I do not have the capacity to calculate the estimate produced by the Stanford graduate students who authored “Going For Broke” but if I apply the same ratio used with CalPERS to MMWD’s unfunded liabilities as they existed at the end of the 2007 fiscal year it looks like this:

Simply put the bill staring the ratepayers of MMWD in the face could be in the neighborhood of $300,000,000! However it is couched, whether by distributing it over thirty years, manipulating it, or massaging it with actuarial assumptions for investment returns, the ratepayers of MMWD will be facing regular rate increases

forever.

For those who feel lost my sympathies are with you; however there is a glimmer of hope. First there is now a lot of attention focused on MMWD and the performance of the board members we have elected to guard our interests. Next, if you travel up 101 north a few miles you will run into the community of Novato and the Novato Sanitary District. I Googled them and the first thing I noticed was their

organization chart. Unlike MMWD’s which has the Board at the top, sitting above the NSD Board of Directors is a box entitled “NSD Ratepayers”. What a novel concept. I knew their Board, over the strong opposition of the unionized work force, had made the decision to contract the operation of a newly completed water treatment facility to an outside company, a move designed to save the ratepayers $7 million over the life of the

5 year contract . It is not without challenges and the biggest is coming from

labor, the root cause of our current problems. But it was a courageous board that voted to eliminate a number of expensive union positions in favor of a lower cost option; outsourcing.

But the most impressive moment for me was a conversation I had with Beverly James, the Engineer-Manager of the district. When I pointed out the problems at MMWD with OPEBs (Other than pension Post Employment Benefits) she said her board has been concerned about them for a long time. Contrast that with the MMWD board's view. From Section F8 of

"Response to Marin County Civil Grand Jury Report on Retire (sic) Health Care" prepared by General Manager Paul Helliker and supported by the current board by a vote of 4-0, "MMWD believes that public agencies should always be prudent when managing public funds. However, MMWD does not think it is beneficial to speculate on what may occur in the future."

While Novato Sanitary is under the same accounting rules governing all public entities for reporting unfunded liabilities, they chose a discount rate of 4%, a number even more conservative than was used in the Stanford brief. They have moved to reduce their exposure to OPEBs by going to a two-tiered system for retiree medical benefits adopting a

defined contribution plan for employees hired after July 1, 2008. The District contributes 1.5% into a 401a for those employees instead of providing a defined benefit. And when the rest of the State was increasing pension benefits to employees, the Board of the Novato Sanitary District held the line at 2% at 55, still generous by private standards but more manageable than most of California. Engineer/Manager James gave credit for the ratepayer centric focus to board president Mike Di Giorgio. Mike, your performance is a shining light in an otherwise dim landscape and Novato you are very fortunate.

So it is clear that competent and responsible individuals exist in the communities they are elected to serve. There are hurdles to overcome. First candidates must be identified, then they must be elected and that seems to be only the beginning as the challenges to the Novato Sanitary District’s board show. But we have been warned ahead of time that

“Eternal vigilance is the price of liberty.”The ratepayers of MMWD deserve better governance and the coming election provides the opportunity to claim it.

________________________________________________

Next: Is the board of MMWD trying to circumvent voters opposed to the desalinization plant with the creation last week of the Marin Municipal Water District Financing Authority?

As we say on the farm, “the chickens eventually come home to roost.” So it is with the Obama health care plan. Last November I pointed out in my blog “Health Care Part II…” that there were two bills introduced by Rep. Nancy Pelosi covering health care.

As we say on the farm, “the chickens eventually come home to roost.” So it is with the Obama health care plan. Last November I pointed out in my blog “Health Care Part II…” that there were two bills introduced by Rep. Nancy Pelosi covering health care.

{kind=link}

{kind=link}